What is a Closing Protection Letter (CPL)?

A closing protection letter (CPL) protects a buyer, lender or seller against losses due to the acts of the title insurer’s named issuing title company.

How does a CPL affect me as a Buyer/Lender or Seller?

The CPL protects you for acts of theft of settlement funds or fraud with regard to settlement funds; and failure to comply with written closing instructions by the proposed insured when agreed to by the title company relating to title insurance coverage. The fee for each CPL is $25.

What are the recent changes in law regarding CPLs?

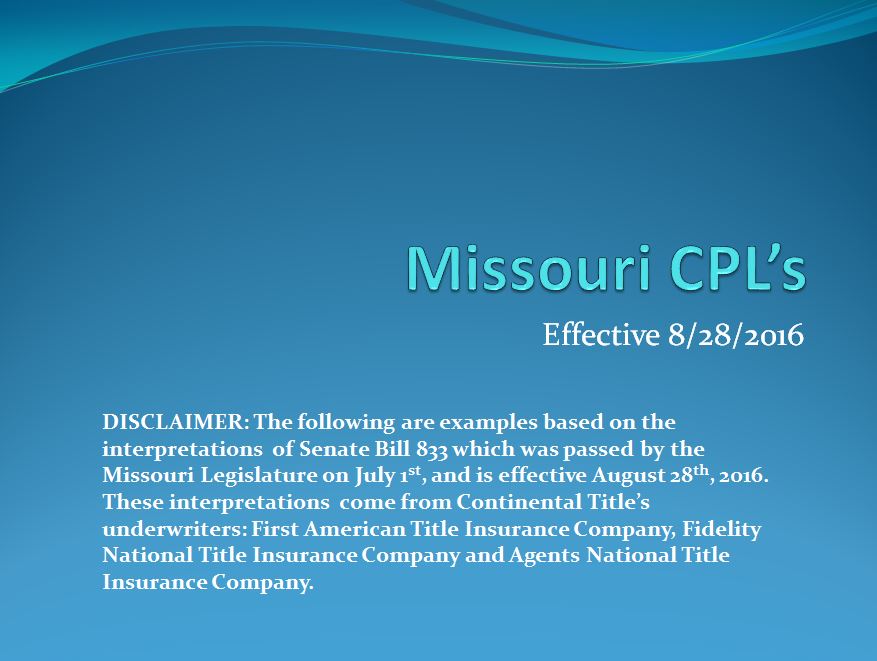

Senate Bill 833 was signed by Governor Nixon and took effect August 28, 2016. The bill requires that a CPL must be issued on all residential transactions where a policy of title insurance is issued and a title agent, agency, or underwriter is handling any funds or documents on behalf of a consumer or lender. The notice of unprotected closing can only be used when the agent, agency, or underwriter is performing escrow functions and a policy of title insurance is not being issued. In many cases, the seller has been signing a notice of unprotected closing at the closing table and waiving a CPL. If there is a policy being issued in the transaction, this is no longer permitted.

What is the history of CPLs?

In 2008 Missouri enacted legislation (SB 66) requiring the issuance of CPLs to buyers and sellers on residential transactions when a licensed title producer provided escrow services and a policy of title insurance was being issued. Interpretation of the statutes led to the conclusion that buyers and sellers could waive the issuance of a CPL. If no CPL was available because no title insurance policy was contemplated, or no title insurance policy was being written by the settlement agent’s underwriter, the DIFP’s T-3 form (Notice of Settlement Risk) would be given in lieu of the CPL. The law, as written, contained potentially confusing provisions in that it seemed to eliminate the requirement for a CPL if one was not requested. There was no requirement for a CPL or T-3 to a lender, although the lender could request one (in which case the buyer could not waive it), and there was no requirement for a CPL to a borrower on a residential refinance transaction.

The CPL law has now been changed in several respects by SB 833, and those changes become effective for all residential closings to which CPLs apply occurring on or after August 28, 2016.

What to know today:

- CPLs can no longer be waived when available.

- CPLs must be issued to all parties (buyers/borrowers, sellers and lenders) when the title company provides escrow services for residential transactions.

- No change has occurred regarding CPLs for non-residential transactions. Residential real estate transaction means the sale, purchase, financing, or refinancing of a house or other dwelling designed principally for the occupancy of from one to four (1-4) families, but does not include transaction involving real estate designed for business, commercial or agricultural purposes. 20CSR 500-7.020.

- CPL practices in connection with split closings require separate consideration.

Further CPL Resources:

Click HERE to download our PowerPoint to review the changes to CPLs.

Please contact us at marketing@ctitle.com with any questions you may have.